TWAPER (Price Feed App)

Twaper is a Muon app to get a token price from decentralized exchanges in a way that is secure against price manipulations. It uses the Uniswap TWAP approach with the following extra benefits over the original on-chain implementation:

It detects and removes outlier prices before calculating averages to prevent price manipulations through applying a sharp rise/fall in the price for a short duration.

In order to reject unexpected price changes, it applies a fuse mechanism that stops the system when a short duration average shows a large price volatility compared to a longer one.

It does not require periodic transactions to register checkpoints on-chain which are costly and hard to maintain.

This document describes how Twaper is developed, and is made up of four sections:

In the first section, we describe how a module is developed to calculate TWAP of a pair of tokens based on the information it gets from a Uniswap pool or one of its forks.

In this section, we explain how to use the module from section one to obtain a token’s price from routes made of pairs that end with a stablecoin. These routes can be in different exchanges on different chains.

In section 3, we demonstrate how the TWAP of an LP token is calculated using the procedure in section 2.

This section explains how a request is processed by the app.

NB: Throughout this document, pair price refers to the price of one token in terms of the other.

Calculating TWAP of a Pair

Obtaining Price Changes

To calculate Time Weighted Average Price for a pair in a time period, the token prices should be obtained for each block in the period. One approach might be to call getReserves for each block, calculate the price for the block by dividing _reserve1 to _reserve0, and calculate the average of all the prices.

Following such an approach is a time-consuming and costly procedure because it requires numerous calls to the blockchain RPC endpoint. For instance, if we need the average for a 30-minute period for a network with 15-second blocks, there should be 120 calls of getReserves.

To solve this problem, a single request is sent to query all Sync events that are emitted each time the reserves are updated due to minting, burning and swapping.

getSyncEvents: async function (chainId, seedBlockNumber, pairAddress, blocksToSeed) {

const w3 = networksWeb3[chainId]

const pair = new w3.eth.Contract(UNISWAPV2_PAIR_ABI, pairAddress)

const options = {

fromBlock: seedBlockNumber + 1,

toBlock: seedBlockNumber + blocksToSeed

}

const syncEvents = await pair.getPastEvents("Sync", options)

When there is more than one change in a block’s reserves, only the final should be considered and the others are excluded.

let syncEventsMap = {}

// {key: event.blockNumber => value: event}

syncEvents.forEach((event) => syncEventsMap[event.blockNumber] = event)

return syncEventsMap

},

Listing the Price for Each Block

Now there is a list of all the blocks in which reserves have changed and the values of the reserves in those blocks for the defined time period. To calculate the TWAP, a list of prices is needed that shows the final price in each block. To generate this list, we require the initial reserve state in the seed block in addition to the list of reserves values.

getSeed: async function (chainId, pairAddress, blocksToSeed, toBlock) {

const w3 = networksWeb3[chainId]

const seedBlockNumber = toBlock - blocksToSeed

const pair = new w3.eth.Contract(UNISWAPV2_PAIR_ABI, pairAddress)

const { _reserve0, _reserve1 } = await pair.methods.getReserves().call(seedBlockNumber)

const price0 = this.calculateInstantPrice(_reserve0, _reserve1)

return { price0: price0, blockNumber: seedBlockNumber }

},

At this stage, the initial state and list of reserves values are available, so the price list can be generated.

createPrices: function (seed, syncEventsMap, blocksToSeed) {

let prices = [seed.price0]

let price = seed.price0

// fill prices and consider a price for each block between seed and current block

for (let blockNumber = seed.blockNumber + 1; blockNumber <= seed.blockNumber + blocksToSeed; blockNumber++) {

// use block event price if there is an event for the block

// otherwise use last event price

if (syncEventsMap[blockNumber]) {

const { reserve0, reserve1 } = syncEventsMap[blockNumber].returnValues

price = this.calculateInstantPrice(reserve0, reserve1)

}

prices.push(price)

}

return prices

},

Each pair is made up of two tokens. To calculate the price of token0 in terms of token1 from the reserves, reserve1 should be divided by reserve0. As there are no floating point numbers in Solidity, and price may be a floating point number, a quotient named Q112 is used to retain the precision of the price by multiplying it by 2^112.

calculateInstantPrice: function (reserve0, reserve1) {

// multiply reserveA into Q112 for precision in division

// reserveA * (2 ** 112) / reserverB

const price0 = new BN(reserve1).mul(Q112).div(new BN(reserve0))

return price0

},

Detecting Outliers

Before calculating the average, prices that are potentially the result of manipulation should be detected and removed from the list. This is technically called outlier detection. At present, a simple algorithm called Z-score is used for outlier detection.

The Z-score measures how far a data point is away from the mean as a multiple of the standard deviation (std). In simple words, it indicates how many standard deviations an element is from the mean, so

z_score = abs(x - mean) / std

This means any price with a Z-score higher than the threshold will be considered an outlier and excluded from the final average.

std: function (arr) {

let mean = arr.reduce((result, el) => result + el, 0) / arr.length

arr = arr.map((k) => (k - mean) ** 2)

let sum = arr.reduce((result, el) => result + el, 0)

let variance = sum / arr.length

return Math.sqrt(variance)

},

removeOutlierZScore: function (prices) {

const mean = this.calculateAveragePrice(prices)

// calculate std(standard deviation)

const std = this.std(prices)

if (std == 0) return prices

// Z score = abs(price - mean) / std

// price is not reliable if Z score > threshold

return prices.filter((price) => Math.abs(price - mean) / std < THRESHOLD)

},

For outlier detection based on Z-score, the price logarithm is used because price is logarithmic in nature. Essentially, using the log of prices can better show the viewer the rate of change over time. If prices are considered linearly, price change from 1 to 2 equals price change from 1001 to 1002. In logarithmic viewpoint, however, these two changes are clearly different.

The process of removing outliers is done twice. Calculating the average including outliers makes the average and the resulting standard deviation biased. Repeating the outlier detection process after cleaning the data set by removing any obviously outlying prices in the first run assures us that more subtle outliers can be detected as well. Although this approach may cause the removal of prices that are not the result of price manipulation, it drastically reduces the chances of not detecting a manipulated price.

removeOutlier: function (prices) {

const logPrices = []

prices.forEach((price) => {

logPrices.push(Math.log(price));

})

let logOutlierRemoved = this.removeOutlierZScore(logPrices)

logOutlierRemoved = this.removeOutlierZScore(logOutlierRemoved)

const outlierRemoved = []

const removed = []

prices.forEach((price, index) => logOutlierRemoved.includes(logPrices[index]) ? outlierRemoved.push(price) : removed.push(price.toString()))

return { outlierRemoved, removed }

},

Now we have all the necessary data to calculate the average. To make the process simpler, only the price of token0 in terms of token1 has been calculated so far. However, each pair is made of two tokens, each of which has a price in terms of the other and is the other’s reverse. Mathematically, the average of the reverses of multiple numbers does not equal the reverse of their average. That is why we need to calculate all the reverses and then their average to obtain the time weighted average price of token1 in terms of token0.

calculateAveragePrice: function (prices, returnReverse) {

let fn = function (result, el) {

return returnReverse ? { price0: result.price0.add(el), price1: result.price1.add(Q112.mul(Q112).div(el)) } : result + el

}

const sumPrice = prices.reduce(fn, returnReverse ? { price0: new BN(0), price1: new BN(0) } : 0)

const averagePrice = returnReverse ? { price0: sumPrice.price0.div(new BN(prices.length)), price1: sumPrice.price1.div(new BN(prices.length)) } : sumPrice / prices.length

return averagePrice

},

Applying Fuse Mechanism

Having removed the outliers, the short-term average is generated. At this stage, a fuse mechanism is implemented, through which the short-term average is compared with a longer-term average that acts as a fuse price. If the result of the comparison shows a large difference, the fuse mechanism stops the system.

The fact that we make use of different methods for the calculation of short and long-term averages heightens the app’s reliability; if there is a bug in one of the methods or an attack that influences one of them, the other can cover it.

checkFusePrice: async function (chainId, pairAddress, price, fusePriceTolerance, blocksToFuse, toBlock, abiStyle) {

const w3 = networksWeb3[chainId]

const seedBlock = toBlock - blocksToFuse

const fusePrice = await this.getFusePrice(w3, pairAddress, toBlock, seedBlock, abiStyle)

if (fusePrice.price0.eq(new BN(0)))

return {

isOk0: true,

isOk1: true,

priceDiffPercentage0: new BN(0),

priceDiffPercentage1: new BN(0),

block: fusePrice.blockNumber

}

const checkResult0 = this.isPriceToleranceOk(price.price0, fusePrice.price0, fusePriceTolerance)

const checkResult1 = this.isPriceToleranceOk(price.price1, Q112.mul(Q112).div(fusePrice.price0), fusePriceTolerance)

return {

isOk0: checkResult0.isOk,

isOk1: checkResult1.isOk,

priceDiffPercentage0: checkResult0.priceDiffPercentage,

priceDiffPercentage1: checkResult1.priceDiffPercentage,

block: fusePrice.blockNumber

}

},

Calculating Fuse Price

To calculate the long-term average needed for the fuse mechanism, we use the off-chain implementation of the exact method that DEXes use to calculate on-chain TWAP.

Some Uniswap forks have made modifications to the on-chain TWAP calculation method originally made by Uniswap. In this app, the original Uniswap version and a well-known fork, Solidly, are implemented.

getFusePrice: async function (w3, pairAddress, toBlock, seedBlock, abiStyle) {

const getFusePriceUniV2 = async (w3, pairAddress, toBlock, seedBlock) => {

...

}

const getFusePriceSolidly = async (w3, pairAddress, toBlock, seedBlock) => {

...

}

const GET_FUSE_PRICE_FUNCTIONS = {

UniV2: getFusePriceUniV2,

Solidly: getFusePriceSolidly,

}

return GET_FUSE_PRICE_FUNCTIONS[abiStyle](w3, pairAddress, toBlock, seedBlock)

},

In this doc, only the original Uniswap implementation is explained. To calculate the long-term average, we make use of the two variables price0CumulativeLast & price1CumulativeLast that are available on the pair contract for on-chain TWAP calculations.

const getFusePriceUniV2 = async (w3, pairAddress, toBlock, seedBlock) => {

...

}

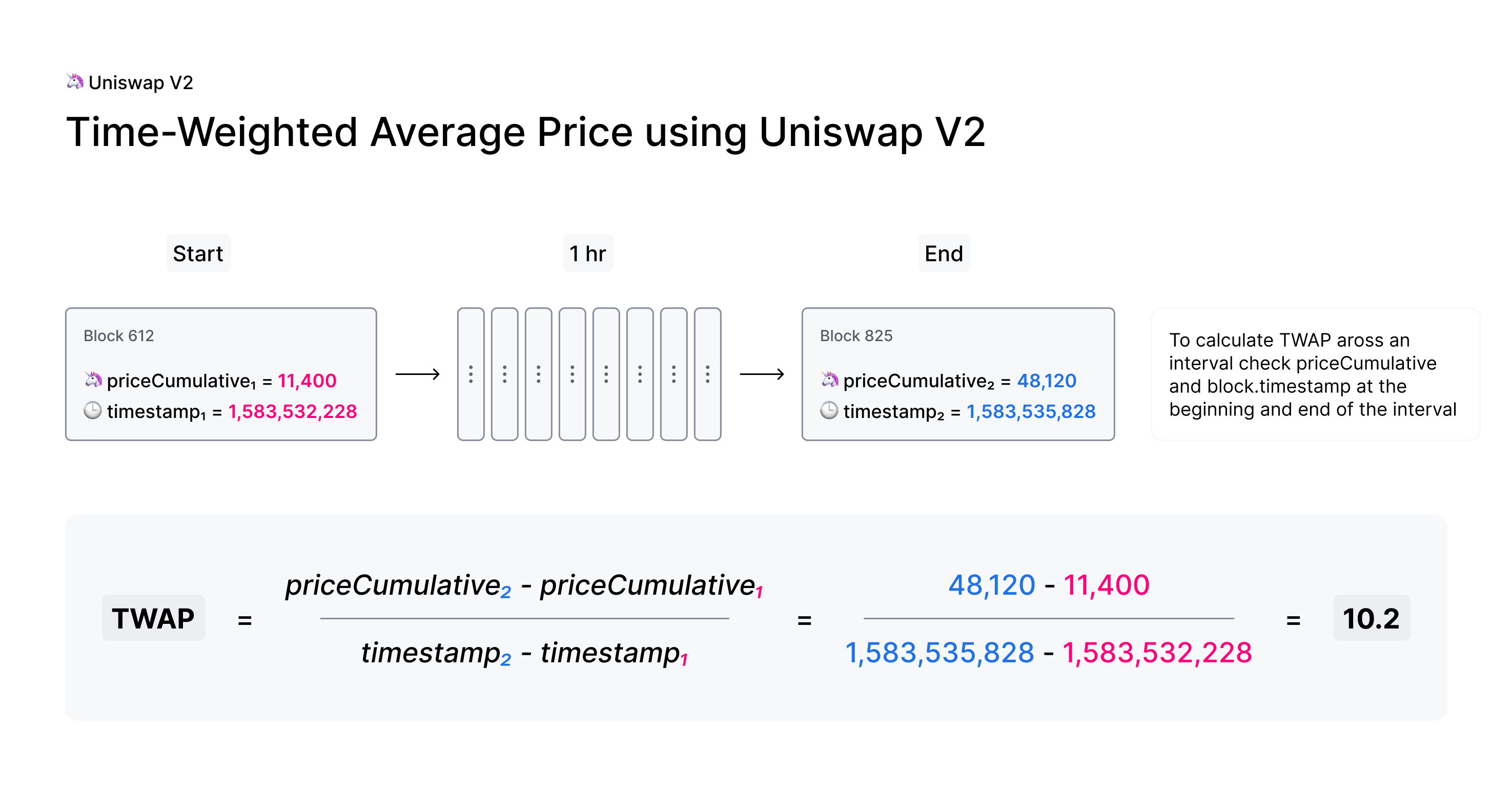

Here is the method that Uniswap has proposed for calculating time-weighted average called V2 solution:

Each time the price changes, it multiplies the previous price by the time period during which that price is valid as the weight of the price. The summation of the results are accumulated in the priceCumulativeLast which is divided by the total time period resulting in the time-weighted average. Uniswap stores and provides the necessary data for this calculation.

The following diagram illustrates how this process works. To get more information, see here.

This is how the Uniswap method is implemented: The time-weighted average can be calculated by dividing the difference of these variables by the blocks’ time difference.

const period = new BN(to.timestamp).sub(new BN(seed.timestamp)).abs()

return {

price0: new BN(price0CumulativeLast).sub(new BN(seedPrice0CumulativeLast)).div(period),

price1: new BN(price1CumulativeLast).sub(new BN(seedPrice1CumulativeLast)).div(period),

blockNumber: seedBlock

}

Updating priceCumulativeLast

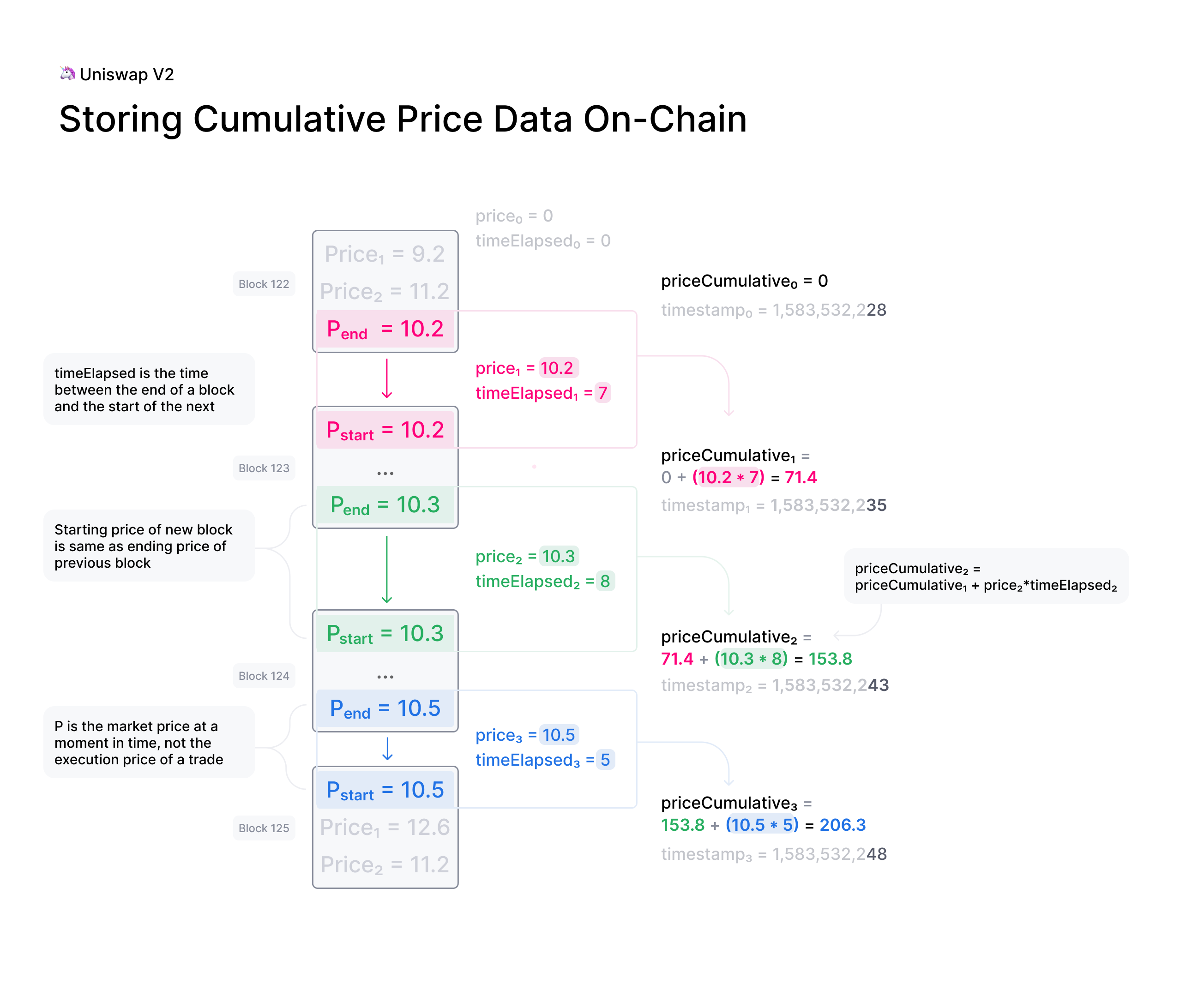

If we are to calculate TWAP for a specified time period, for instance the last 24 hours, it seems that the difference between priceCumulativeLast for the current and starting blocks should be divided by 24 hours. In reality, however, the priceCumulativeLast is only updated with each swap, so when this variable is queried for a block, its value may belong to a few blocks earlier, that is, the block when a swap took place. To obtain the accurate value of the variable for a block, the block price should be multiplied by the time period between the last swap and block, and the result should be added to the value of priceCumulativeLast from the last swap.

updatePriceCumulativeLasts: function (_price0CumulativeLast, _price1CumulativeLast, toBlockReserves, toBlockTimestamp) {

const timestampLast = toBlockTimestamp % 2 ** 32

if (timestampLast != toBlockReserves._blockTimestampLast) {

const period = new BN(timestampLast - toBlockReserves._blockTimestampLast)

const price0CumulativeLast = new BN(_price0CumulativeLast).add(this.calculateInstantPrice(toBlockReserves._reserve0, toBlockReserves._reserve1).mul(period))

const price1CumulativeLast = new BN(_price1CumulativeLast).add(this.calculateInstantPrice(toBlockReserves._reserve1, toBlockReserves._reserve0).mul(period))

return { price0CumulativeLast, price1CumulativeLast }

}

else return { price0CumulativeLast: _price0CumulativeLast, price1CumulativeLast: _price1CumulativeLast }

},

Obtaining the Pair Price

All the procedures explained above in a step-by-step manner can now be reviewed in the implementation of calculatePairPrice function.

The price of the starting block for the period for which the average is to be calculated is obtained by

getSeedfunction.The list of

Syncevents for the period is obtained by thegetSyncEventsfunction.The price list is generated by the

createPricesfunction.Any outliers are removed using

removeOutlierfunction.The average price is calculated through

calculateAveragePricefunction.The fuse mechanism is triggered by the

checkFusePricefunction if there is a large difference between the short and long-term averages.

calculatePairPrice: async function (chainId, abiStyle, pair, toBlock) {

const blocksToSeed = networksBlocksPerMinute[chainId] * pair.minutesToSeed

const blocksToFuse = networksBlocksPerMinute[chainId] * pair.minutesToFuse

// get seed price

const seed = await this.getSeed(chainId, pair.address, blocksToSeed, toBlock)

// get sync events that are emitted after seed block

const syncEventsMap = await this.getSyncEvents(chainId, seed.blockNumber, pair.address, blocksToSeed)

// create an array contains a price for each block mined after seed block

const prices = this.createPrices(seed, syncEventsMap, blocksToSeed)

// remove outlier prices

const { outlierRemoved, removed } = this.removeOutlier(prices)

// calculate the average price

const price = this.calculateAveragePrice(outlierRemoved, true)

// check for high price change in comparison with fuse price

const fuse = await this.checkFusePrice(chainId, pair.address, price, pair.fusePriceTolerance, blocksToFuse, toBlock, abiStyle)

if (!(fuse.isOk0 && fuse.isOk1)) throw { message: `High price gap 0(${fuse.priceDiffPercentage0}%) 1(${fuse.priceDiffPercentage1}%) between fuse and twap price for ${pair.address} in block range ${fuse.block} - ${toBlock}` }

return {

price0: price.price0,

price1: price.price1,

removed

}

},

Calculating TWAP of Routes

Very often, the dollar-based price of a token cannot be obtained from a pair because many of the important pairs do not contain stablecoins; that is, both tokens are volatile. For instance, on mainnet, numerous pools with large liquidity for many tokens have WETH as their counterpart. The same goes for tokens on other chains and their native tokens. That is why to get the dollar-based price of a token, we usually need to calculate the price of a route of pairs.

Imagine there is a pair between token A and WETH, and the price of A is 0.02 in terms of WETH. There is also a pair between WETH and USDC, and the price of WETH is, for example, 1,500 in terms of USDC. Therefore, we can get the price of A in terms of USDC by multiplying the prices of the two pairs in the route, which comes to $30.

Our price feed app, TWAPER, makes use of the module explained in section 1 to calculate the price of a pair.

module.exports = {

...Pair,

APP_NAME: 'twaper',

...

},

Calculating Prices of Routes

To calculate the TWAP of a route, the prices of pairs forming it should be calculated.

Instead of calculating the price for each pair separately, we obtain all the prices for the pairs of all routes asynchronously through Promise.

const promises = []

for (let [i, route] of routes.entries()) {

for (let pair of route.path) {

promises.push(this.getTokenPairPrice(route.chainId, route.abiStyle, pair, toBlocks[route.chainId]))

}

}

let result = await Promise.all(promises)

At this stage, the TWAP of a route is calculated by multiplying the prices of pairs together.

let price = Q112

...

for (let pair of route.path) {

price = price.mul(result[0].tokenPairPrice).div(Q112)

...

}

Now that the price of a token for one single route is calculated, we can calculate the time weighted price average for different routes based on the weights read from config, which will be described in the next section. These routes may be on one exchange or different exchanges on one chain or even different exchanges on different chains.

calculatePrice: async function (validPriceGap, routes, toBlocks) {

let sumTokenPrice = new BN(0)

let sumWeights = new BN(0)

let prices = []

const removedPrices = []

...

for (let route of routes) {

let price = Q112

...

for (let pair of route.path) {

price = price.mul(result[0].tokenPairPrice).div(Q112)

routeRemovedPrices.push(result[0].removed)

result = result.slice(1)

}

sumTokenPrice = sumTokenPrice.add(price.mul(new BN(route.weight)))

sumWeights = sumWeights.add(new BN(route.weight))

prices.push(price)

removedPrices.push(routeRemovedPrices)

}

...

return { price: sumTokenPrice.div(sumWeights), removedPrices }

},

When there are several routes and there is a big difference between the obtained maximum and minimum prices, we have implemented another fuse mechanism to stop the system.

if (prices.length > 1) {

let [minPrice, maxPrice] = [BN.min(...prices), BN.max(...prices)]

if (!this.isPriceToleranceOk(maxPrice, minPrice, validPriceGap).isOk)

throw { message: `High price gap between route prices (${minPrice}, ${maxPrice})` }

}

Loading the Configuration

There is a question of where and how the required configurations for the price calculation is obtained; configurations such as which routes are used and which pairs are the routes composed of. To define the required configuration, the ConfigFactory smart contract is used. The ConfigFactory generates a contract which should be fed the necessary parameters.

For more detailed information about ConfigFactory see here. The verified deployment of this contract on Fantom can be seen here.

The ConfigFactory has a method called deployConfig that enables users to deploy new Config instances for their tokens’ configurations. Each Config has a setter and a validPriceGap that defines the maximum allowed price difference between the routes. The Config contract has an addRoute method that enables the setter to add a route to the Config. A route has a chain ID, a dex, a weight, and a list of pairs. Each pair has a specified period for average calculation, a long-term period and an accepted tolerance for the fuse mechanism, and a reverse flag that specifies whether to use the price of token0 or token1 of the pair. Every config deployment has an address that our app uses to load the required configuration from by calling getRoutes function.

getRoutes: async function (config) {

let configMetaData = await ethCall(config, 'getRoutes', [], CONFIG_ABI, CHAINS.fantom)

return this.formatRoutes(configMetaData)

},

Calculating the TWAP of an LP Token

The TWAPER makes use of the following formula to calculate the TWAP of an LP token.

In the formula, p0 and p1 are the fair prices of the two tokens that the LP represents and are obtained in the method described in section 2; K is a constant that is the result of multiplying the reserves of the two tokens and L is the LP’s total supply. The values for K and L are obtained from the LP’s contract. More details about this formula can be found in the Pricing LP Tokens article.

By using Promise and calculatePrice, values for price0 and price1 are calculated simultaneously. K and L are read from the LP’s smart contract. Having obtained these values, the TWAPER can now calculate the TWAP of the LP.

calculateLpPrice: async function (chainId, pair, routes0, routes1, toBlocks) {

// prepare promises for calculating each config price

const promises = [

this.calculatePrice(routes0.validPriceGap, routes0.routes, toBlocks),

this.calculatePrice(routes1.validPriceGap, routes1.routes, toBlocks)

]

let [price0, price1] = await Promise.all(promises)

const { K, totalSupply } = await this.getLpTotalSupply(pair, chainId, toBlocks[chainId])

// calculate lp token price based on price0 & price1 & K & totalSupply

const numerator = new BN(2).mul(new BN(BigInt(Math.sqrt(price0.price.mul(price1.price).mul(K)))))

const price = numerator.div(totalSupply)

return price

},

Like regular tokens, LP tokens have a config that includes routes for token0 and token1. The config is obtained by calling getMetaData function from the LpConfig contract. To deploy LpConfig, the function deployLpConfig is called from ConfigFactory. More details can be found here.

Handling the Request

Now that all the different components of the app have been explained in a step-by-step manner, it is time to review the implementation of the onRequest function that is the entry point of requests to the Muon app.

The first action is to determine which method - price or lp_price - is to be used. Regardless of the method, the two parameters should be sent to the app: the contract address from which the config loads, and the toBlocks for which the average is to be calculated.

onRequest: async function (request) {

let {

method,

data: { params }

} = request

switch (method) {

case 'price':

let { config, toBlocks } = params

...

case 'lp_price': {

let { config, toBlocks } = params

...

}

default:

throw { message: `Unknown method ${params}` }

}

},

The toBlocks parameter is optional and if it is not sent to the app, it means the price for the current block should be calculated.

// prepare toBlocks

if (!toBlocks) {

if (!request.data.result)

toBlocks = await this.prepareToBlocks(chainIds)

else

toBlocks = request.data.result.toBlocks

}

else toBlocks = JSON.parse(toBlocks)

However, as the latest block may be reorged and we need to assure all nodes are using the same block, we apply a number of blocks for confirmation; that is, rather than assigning the current block to the toBlock, a block that is a few blocks before the current one is assigned.

getReliableBlock: async function (chainId) {

const latestBlock = await ethGetBlockNumber(chainId)

const reliableBlock = latestBlock - blocksToAvoidReorg[chainId]

return reliableBlock

},

prepareToBlocks: async function (chainIds) {

const toBlocks = {}

for (let chainId of chainIds) {

// consider a few blocks before the current block as toBlock to avoid reorg

toBlocks[chainId] = await this.getReliableBlock(chainId)

}

return toBlocks

},

Method: price

If the method is price, the function getRoutes is called to obtain routes & chainIds.

const { routes, chainIds } = await this.getRoutes(config)

With routes and toBlocks, the price average of different routes are calculated using calculatePrice, as explained above.

const { price, removedPrices } = await this.calculatePrice(routes.validPriceGap, routes.routes, toBlocks)

Finally, the timestamp at which the price is calculated should be returned to the app. This enables the app to ensure that the price is not an expired one.

// get earliest block timestamp

const timestamp = await this.getEarliestBlockTimestamp(chainIds, toBlocks)

return {

config,

routes,

price: price.toString(),

removedPrices,

toBlocks,

timestamp

}

Because routes are on different chains and are assigned to different toBlocks, the earliest timestamp is returned.

getEarliestBlockTimestamp: async function (chainIds, toBlocks) {

const promises = []

for (const chainId of chainIds) {

promises.push(ethGetBlock(chainId, toBlocks[chainId]))

}

const blocks = await Promise.all(promises)

const timestamps = []

blocks.forEach((block) => {

timestamps.push(block.timestamp)

})

return Math.min(...timestamps)

},

Method: lp_price

If the method is lp_price, the function getLpMetaData is called to obtain the chainId, pair, config0 & config1.

let { chainId, pair, config0, config1 } = await this.getLpMetaData(config)

The variables config0 & config1 should be changed to routes0 & routes1 as follows so that they can be used by calculateLpPrice.

let { routes: routes0, chainIds: chainIds0 } = this.formatRoutes(config0)

let { routes: routes1, chainIds: chainIds1 } = this.formatRoutes(config1)

Now that routes for token0 and ``token``1 are obtained, the LP price can be calculated.

const price = await this.calculateLpPrice(chainId, pair, routes0, routes1, toBlocks)

Here, the same points apply to the timestamp as the other method except for the return values, as shown below:

// get earliest block timestamp

const timestamp = await this.getEarliestBlockTimestamp(chainIds, toBlocks)

return {

config,

price: price.toString(),

toBlocks,

timestamp

}